In this article, I’ll discuss how you can use a HELOC loan as your savings account and emergency fund to dramatically reduce the interest paid and the length of your mortgage. We’ll run through the numbers on how you can pay-off your mortgage in 4 years, and set up a personal HELOC bank for life.

Magic HELOC Math – Setting Up Your Personal Bank

I stumbled across this bit of financial wizardry when one of my friends mentioned that someone in their church was doing a wealth class on how to pay-off your mortgage in 4 years using a HELOC.

I am attracted to interesting personal finance ideas like trekkies to a Spock costume at Comic-Con, so I dug into the numbers.

There were a few books on the topic, and I found one to that gave an overview of the concept: How To Pay Off Your Mortgage In Five Years (Amazon Link). However, none of them provided the resources I needed to apply the concept to my situation, so I built my own spreadsheet (Available for Download Here).

The math ended up being, let’s say, tricky. I iterated through a few spreadsheets and simulated the pay-off between a HELOC and a mortgage loan to ultimately confirm that the strategy worked.

This article will explore my findings and give you a snapshot of how to set up your very own HELOC Bank. This strategy dove tails nicely with an improved version of the concept of Infinite Banking which I plan to delve into more in a future article.

Author’s Note: If you read the above book, I would suggest you DO NOT invest in whole life insurance to accomplish the Infinite Banking strategy. It doesn’t make sense for most people since the whole life insurance is a drag on return.

However, I’m getting ahead of myself. Get started by reading the article below. Enjoy!

Core Premise: Build Your Personal Bank

Owning your own bank is a concept that says you should avoid unproductive debt or buying things that you didn’t first save to get. The best way to save money isn’t by storing it in a checking or savings account. That’s unproductive money meaning it gets eaten away by inflation and doesn’t earn you much of anything.

Instead, you want to setup a “personal bank” where you can invest that money but have a line of credit at a lower interest rate than what the investment makes you. That means the investment is always earning more than the cash you pull out of the line of credit.

It’s a little complex, but read that sentence over until it clicks.

By finding an investment that allows you to earn a return on that money while keeping the equity liquid it can serve as a savings account, emergency fund, or for large purchases (a car, a house, a rental…etc).

When you pull money out of one investment to invest in another, that means the same money is working in two different assets and thus boosts your return.

People commonly “buy on margin” (that’s another term for this same thing) in this fashion with whole life insurance policies, stocks, retirement accounts, and houses. The best way I’ve found to accomplish this for the average person is the HELOC Personal banking strategy described in this article.

The second benefit is obviously, it pays off your mortgage FAST.

A HELOC with a simple interest rate can be strategically used to pay off a primary amortized mortgage in 4 years. The way this works is you dump your savings and emergency fund into your mortgage then use a HELOC as your emergency fund. Using this HELOC Strategy, homeowners can drastically shorten the loan term, increase their home equity, and save a substantial amount of money on interest charges and fees. Your house thus becomes your personal bank and replaces your need for storing large amounts of cash in a savings account, checking account, or keeping a lot of liquid money for an emergency fund.

To kick off our discussion let’s talk about the difference between an Amortized mortgage and a HELOC simple interest mortgage.

In the next section, I’m going to run through a quick summary of what an amortized mortgage is, what a HELOC is and how this strategy works.

What is an Amortized Mortgage?

An amortized mortgage is where the borrower makes regular payments that include both principal and interest usually for a 15 yr or 30 yr period. Each payment reduces the loan balance and pays interest on the outstanding loan principal. This results in a gradual reduction of the debt over time until the debt is paid off completely by the end of the loan term.

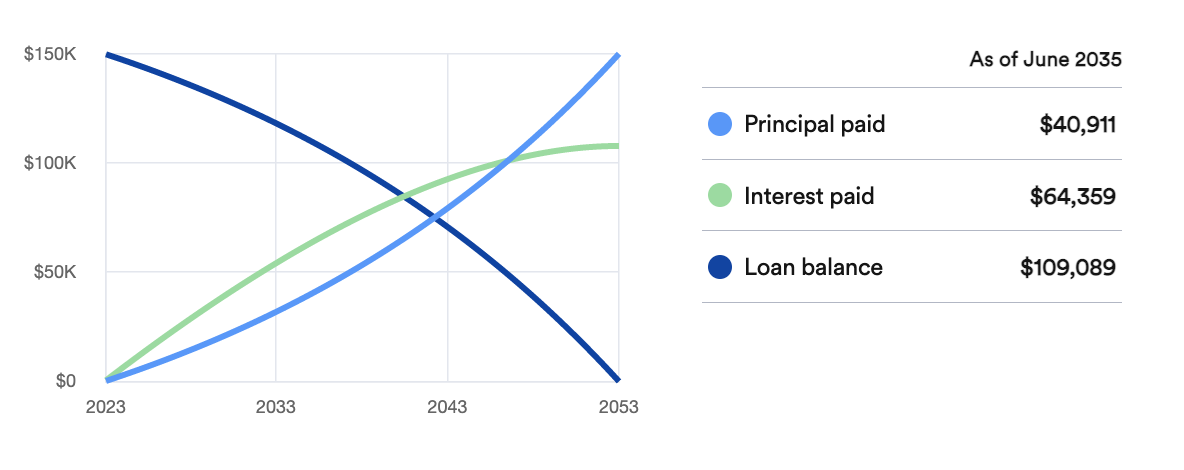

For example, let’s say a borrower takes out a 30-year fixed-rate mortgage for $150,000 at an interest rate of 4%. Using an amortization schedule, the monthly payment would be calculated to include both principal and interest, resulting in a fixed monthly payment of approximately $716.

Figure A gives you the key variables we’ll be using for our mortgage and our upcoming example:

Figure A: Amortization Summary $150,000 30-year 4% Mortgage (source: bankrate.com)

The below amortization schedule illustrates the first 20 monthly payments for this mortgage. The important thing to notice is how little principle is being paid off initially without using our HELOC strategy. This is the key insight that gives the strategy so much power.

Figure B: Amortization Summary $150,000 30-year 4% Mortgage (source: bankrate.com)

What is a HELOC Loan?

HELOC stands for Home Equity Line of Credit. It is a type of loan that allows homeowners to borrow money using their home’s equity as collateral. Home equity is the difference between the current value of a home and the outstanding mortgage balance that you owe. The greater the equity, the greater the amount of a HELOC that you can apply for.

A HELOC works similarly to a credit card. The borrower is approved for a credit limit and can borrow and repay money as needed, up to that credit limit. The borrower can access the funds through a check, bank account, or credit card provided by the lender. Most important for our purposes, and unlike amortized loans, HELOCs are only charged interest on the amount borrowed. That means you can pay-off as much or as little of the principle as you want.

This is important to the HELOC Bank Strategy, so let’s come back to that.

Amortized Mortgage vs HELOC Loan

Figure C: Amortization Summary $150,000 30-year 4% Mortgage (source: bankrate.com)

The table above reiterates a unique insight that’s core to the HELOC Bank Strategy. Amortized payments frontload interest and backload principle. By percentage, the interest paid is the same through the length of the loan, but in practical numbers, the amount owed is a lot more at the front, so the interest paid is a lot more too. In order to make a fixed monthly payment, that means you have to make the initial interest high and the initial principal pay-off low.

Gradually as you pay down the loan, more principle gets paid off an less of your payment goes toward interest.

This benefits the bank since they’ll earn most of their income off the loan up front. Since the median time Americans stay in a house is 13 years, people often upgrade or change houses before paying off the majority of their mortgage.

The flip side is also true. If you can pay-off more of your principal early on, then there are HUGE interest savings over the length of the loan. That’s where the HELOC magic begins.

The strategy seems like magic because it’s not intuitive how the HELOC strategy can pay-off your mortgage 26 years early without costing you extra but the math works.

By dumping all your savings and your entire emergency fund into your mortgage and using your HELOC as your savings and emergency fund, you critically pay-off a lot of the principle and subsequently reduce your interest paid significantly.

In this scenario, your HELOC equity ends up operating like a high interest savings account saving you the interest you would have otherwise paid to a bank. Oftentimes, that mortgage interest is a higher interest rate than you would get in a high interest savings account.

When I ran the numbers on adding a line of credit to my rental, at the time of this writing, I essentially earned 5% interest on the money I had stashed in my house when fully paid off compared to 3.25% in a high interest savings account.

This ends up being a bank replacement strategy, and can conveniently pay-off your mortgage in 4 years.

There are a few key differences between the HELOC strategy and other alternatives.

- Flexibility – HELOC vs Amortized Mortgage: The amortized mortgage provides a set payment. That means high interest up front, and the same cash flow cost through the length of the loan. It also doesn’t give you the flexibility of a HELOC to borrow from it whenever you want or to suspend payments for a period and accrue interest. A HELOC would let you pull cash out to buy a car or a new rental property. Then you could setup your desired payment back into the HELOC.

- Liquidity – HELOC vs Amortized Mortgage: The ability to borrow off the equity in your house is one of the critical benefits of the HELOC loan. What you don’t want is to put all your savings and emergency fund into your house and not be able to get it out when there’s an emergency which is what paying off an amortized mortgage would do.

- HELOC vs High Interest Savings: The real alternative to a HELOC banking strategy is a high interest savings account. I setup this HELOC concept on a rental I own. My rental HELOC cost more to get started and required a 20% downpayment on the house. However, you can sidestep all those costs if you already have equity in your home, so it’s usually no added cost and essentially earns you the interest rate that you normally pay on your mortgage. In return for my HELOC, I got a higher ROI and an inflation hedge compared to a high interest savings account. When paid off, my rental house can still offer a 5%+ ROI and when leveraged, I can get a 15%+ ROI. The ROI on a cash flowing rental house pays me a return on the cash in the house, but when I pull the debt out, it can earn me additional money on whatever asset I purchase with it. I love using cash in multiple places to multiply my return on investments.

Case Study Example

I prepared an example of the concept in action and a companion spreadsheet (available for download here) to demonstrate the effectiveness of using this Personal Banking Strategy to pay off your mortgage in 4 years and setup your personal bank. Below I copy the same key variables I mentioned above that we’ll be using for the case study to walk through how the strategy allows you to rapidly pay down your mortgage and setup your personal bank.

Figure D: Case Study Assumptions

Using the median college educated earner’s salary, and estimating a high savings rate of 30%, we’re able to walk through the process to dump all your extra savings into your mortgage and pay it off in 4 years. The goal is much larger than paying off your mortgage since this will provide you dry powder and the equivalent of a high interest savings account you can use across all your investments.

To work through this case study, we will need two debt schedules running in parallel. One for the primary mortgage and one for the HELOC.

For our numbers, the monthly savings from income will be poured into paying down the mortgage along with what you’d normally pay toward your monthly expenses (utilities, groceries…etc). This means you’re storing all your expenses in your HELOC rather than paying them off with cash. Then once that mortgage is paid off, your savings rate is applied to the HELOC balance and you start paying your monthly expenses again as you normally would. Once this HELOC balance is paid off, no additional HELOC funds will be borrowed.

Confusing, right?

Essentially what you’d do to accomplish this is dump all your money into the mortgage (life savings, emergency fund, ongoing savings, personal expenses …etc), and pay off new expenses with a credit card. Then pay off that credit card with your HELOC each month so you don’t get charged the high credit card interst rate. Your goal is moving debt from your amortized mortgage to your HELOC, and putting all your savings into your house equity.

This pays off the mortgage principle fast, and your HELOC has the flexibility to hold debt and roll interest payments back into the HELOC. That means you don’t have to increase your total house payment. However, since your money is liquid via the HELOC line of credit, you can store all extra money in your HELOC, and only pull out equity when you need to for real life expenses.

Below is the amortization table illustrating the initial months payment on the primary mortgage until it’s paid off.

As illustrated, the emergency fund, the combined savings rate, and all your personal expenses are used as an initial Extra Principal to pay off the mortgage balance. This balance is quickly paid off by Month 18.

The key here is that all personal expenses, credit cards, and individual spending gets paid with the HELOC funds. The HELOC interest payments are then rolled into the HELOC account to keep your mortgage payment the same. To the extent that the HELOC expires during this time or that you reach your maximum balance, you would need to either refinance or negotiate new payment terms.

The key take away here is that this payment stream allows you to pay-off the mortgage extremely fast – a year and a half – while moving this debt into a more flexible HELOC.

So, now that we have shown how the primary mortgage can be paid off using the combined Savings Rate/HELOC funds, we will then turn the same monthly payments and all your savings toward paying off the HELOC balance.

The table below illustrates the HELOC amortization schedule for the first 24 months.

Figure F: HELOC Amortization Schedule (First 24 Months)

The HELOC balance begins as $4,695.83 at Month 1 and then increments by this same amount each month for the first 17 months, right before the primary mortgage is paid off.

At this point, we no longer need to add debt into the HELOC. Instead the monthly savings rate along with the monthly mortgage payment are combined to payoff the decreasing interest payments and begin to payoff the HELOC balance.

Therefore, during Month 18, the HELOC balance will begin to be paid back, and you continue this payment process until the entire HELOC balance is paid off.

Combined, all these actions allow you to pay-off your mortgage in just under four years (month 47) as illustrated below.

Figure G: HELOC Amortization Summary Final 30 Months

Throughout this process, your home equity operates as a high interest rate savings account that saves you the cost of the mortgage interest. It also provides you flexibility to keep dry powder for investing when the right opportunities come along. You can invest in real estate with your home equity as the down payment or buy a small business (See Our Fast FI Investing Methodology). Ultimately, you’ll earn a good return on your savings stored in your house while paying yourself first rather than the bank with your home equity.

This HELOC strategy gives you a financing vehicle that operates like your own personal bank account.

This results in you getting the benefits of a real estate hedge against inflation while also letting you invest generally 85% of the equity in a home in higher returning assets. You can also keep the money in liquid equity as the equivalent of a high interest savings account, and pull cash out as needed at the cost of your HELOC interest rate.

This proposed HELOC Banking Strategy also saves you a ton of interest. By paying this balance off in just 4 years, there was only a total of $10,553.33 in combined interest paid.

Note that this combined interest is a whopping $97,251 less than the interest that would have been paid out over the 30 year life of the primary mortgage.

Quite the savings.

Conclusion

The HELOC Personal Bank Strategy offers a path to pay off your mortgage in 4 years, super charge your investing strategy, and create a personal bank you can draw from when you need a loan.

Hopefully, you enjoyed learning about that strategy as much as I did. If you’d like to get into the details on how to implement the concepts shared in this article, check out our HELOC Personal Banking Spreadsheet that you can download here.

In our spreasdheet, we offer a set of master variables you can change that will then update the timeline to paying off your mortgage, your amortization table(s) and your ongoing payments. This sheet will help you implement your very own HELOC Personal Banking Strategy as well as provide a helpful tool to calculate your own numbers.

I like to end my articles on a quote to make you think and Benjamin Franklin has some of the best in wise financial stewardship.

“Beware of little expenses, a small leak will sink a great ship.”

Benjamin Franklin – Poor Richard’s Almanac

What’s the next step you need to take to financial freedom?